- HomeTake me back

- InsuranceSR22, Travel, Gap & More

- About UsWe're here for you!

- Latest NewsPublications

- Contact UsGet started today!

Tel: (972) 386-4386

(800) 967-4386

(800) 967-4386

As I explained in Part 2 of this series, if you already have your automobile insurance through a “high-risk” company it is usually a better option for you to contact your existing insurance agent about providing the SR-22. However, if you are currently insured through a “standard” or “preferred” carrier then it is usually a better option to obtain the SR-22 from a secondary, outside source. However, if this is not done properly it could create some problems that have the potential of being financially devastating.

Without proper guidance, many people will simply turn to the first insurance agency they see advertising SR-22s and ask to purchase the form as inexpensively as possible. The agency will then typically issue a minimum-limits liability-only policy (because this is the least expensive coverage required to issue the SR-22) on whatever vehicle the person happens to be driving that day. The agency is happy because they have sold a policy and the person is happy because they have the form they need; the problem is that the person has now automatically terminated his current insurance coverage on that vehicle through his “preferred” carrier and replaced it with this minimum-limits liability-only policy. Imagine the problems this could cause if there is an auto accident and the person discovers there is no longer coverage for the damage done to his vehicle, or coverage protecting the lien-holder if the vehicle is financed, or any liability loss that exceeds the state minimum limits, or car rental, or towing coverage, etc…

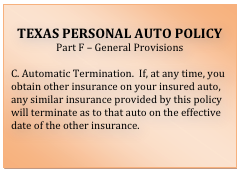

The problem lies in the Texas Personal Auto Policy (see text insert for exact wording). You see, a person can be listed on multiple policies as a driver but a vehicle can only be listed on one policy at a time… if you start a policy on a vehicle it actually voids all prior coverage on that vehicle. This rule is in the policy to prevent someone from committing insurance fraud by purchasing multiple policies on a vehicle, then staging an accident and filing multiple claims for the same loss. This rule only applies to the single vehicle listed on the new policy and would have no effect on any additional vehicles listed on the original policy.

Although this might seem to present an insurmountable dilemma, this situation can be easily solved by purchasing the SR-22 attached to an Operator’s Policy (also commonly referred to as a Non-Owner’s Policy). Instead of providing coverage on a specific listed vehicle, this type of policy is written on the person as a driver. Because it does not provide duplicate coverage on a vehicle already insured on another policy, it completely avoids the Automatic Termination rule in the Texas Personal Auto Policy.

It is important to understand that the Operator’s Policy does not replace your regular auto insurance coverage; it is simply an additional policy that covers you while driving in very specific and limited circumstances. For example, the Operator’s Policy would not provide any coverage for a vehicle you own, rent or lease. Nor would it cover any vehicle that is provided for your regular use or is driven in the course of your employment. It is designed to provide liability coverage for damage you cause while driving a vehicle that you do not own and is not available for your normal use. However because the coverage is so limited, the cost of an Operator’s Policy is generally more affordable than many other options.

Sometimes locating a company willing to issue an Operator’s Policy is not that easy. I occasionally have my clients tell me they were informed by another insurance agent that they could not purchase a Non-Owner’s or Operator’s policy because they own a vehicle. I believe there are a couple of different reasons why someone might be told this. First, it is entirely possible that the insurance company that agent represents does not allow an Operator’s Policy to be issued if the applicant owns a vehicle due to that company’s underwriting guidelines. That is not a state regulation but simply a company policy determining what type of risk that particular company either will or will not accept. Secondly, some agents view the SR-22 as an opportunity to take over a substantial portion of that family’s insurance business. They understand the effects an SR-22 can have on a family’s policies (as I discussed in Part 2 of this series), especially if they are currently insured with a “preferred” company. They see the requirement for the SR-22 as a way to get their “foot in the door” and possibly convince the family to change insurance agents. As a rule of thumb, if an agency wants you to provide information about a vehicle… they are NOT! offering to sell you an Operator’s policy.

Please understand that the use of a Non-Owner’s or Operator’s policy is not the perfect solution for everyone needing an SR-22. If you have a vehicle that is not currently insured, then the best solution for you is to go to an agent that specializes in SR-22s and purchase an SR-22 policy that will cover your automobile. If you currently have insurance coverage through a “non-standard” or “high-risk” company, then your best option would be to contact your agent about adding the SR-22 to your existing policy. However, if you are currently insured through a “standard” or “preferred” carrier and do not want anything to disrupt your existing coverage, then the Non-Owner’s or Operator’s policy could be the best option for you.

Additionally, there are instances where the Operator’s Policy would be the only option available to you if you are required to file an SR-22. For example; if you do not own a vehicle but occasionally drive borrowed autos, you would need to purchase an Operator’s policy in order to obtain the SR-22 form. Another example would be a scenario in which the only vehicle you regularly drive is provided for your use by your employer. That vehicle would typically be insured under a commercial or business policy which would not normally be able to provide the SR-22.

In the next part of this series, I will be discussing the likelihood of your current insurance carrier finding out about the SR-22.

Part 1 | Part 2 | Part 3 | Part 4 | Part 5

Jay Freeman is the owner of ConceptSR22.com, a website specialized in solving Texas SR-22 problems. If you need assistance in obtaining a Texas SR-22 or have questions not addressed in this series, please contact his office from the website. Thank you for reading this series..

© Jay Freeman – This article may be copied and distributed with original attribution and permission of author.

Accurate Concept Insurance

972-386-4386 ~ 800-967-4386

Serving Texas since 1993